India’s 1st Startup Consulting Company Earns YouTube Silver Button

India’s 1st Startup Consulting Company Earns YouTube Silver Button

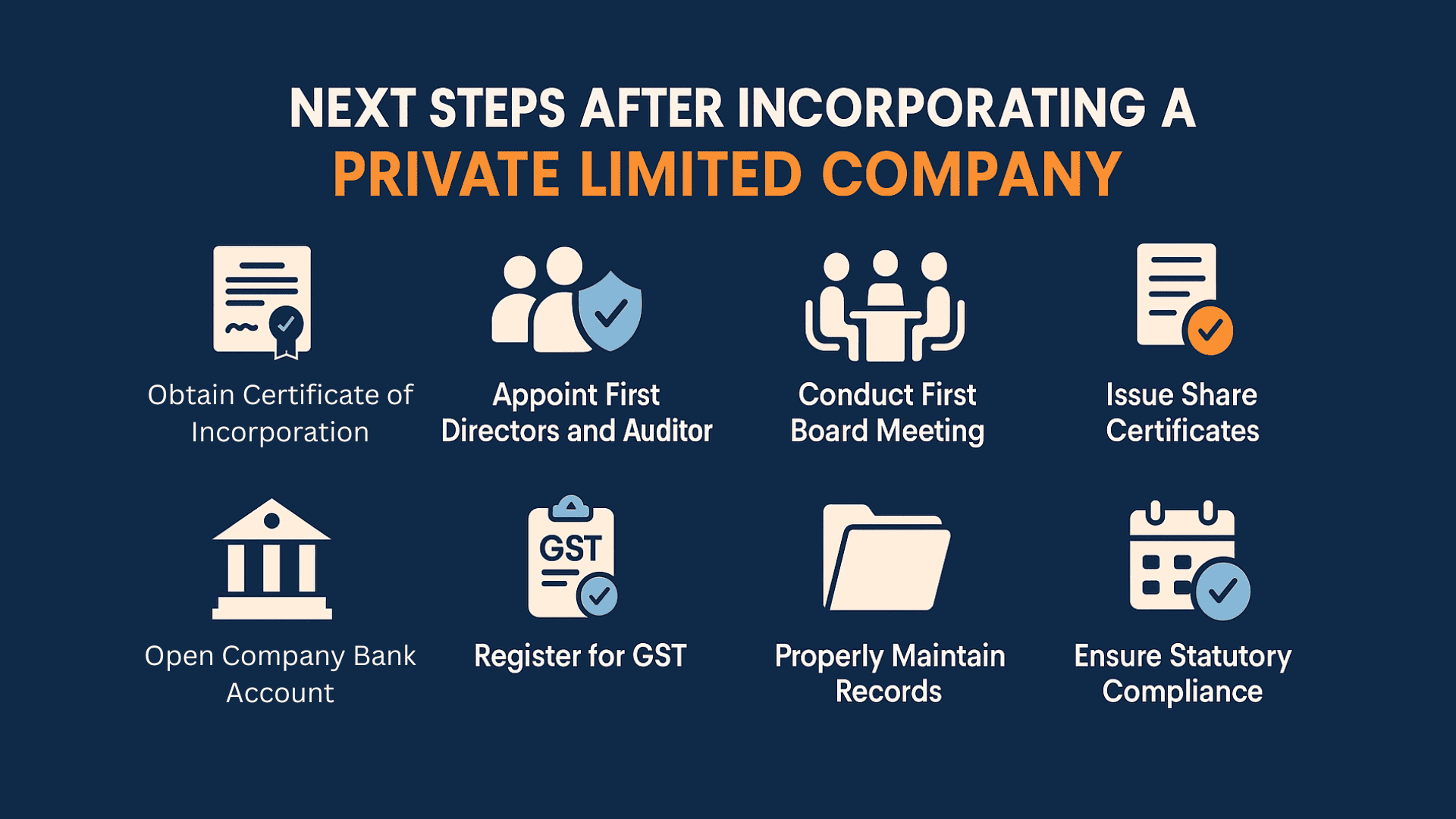

Setting up a Private Limited Company in India is an exciting first step toward starting your business journey. But the process doesn't stop after you receive your Certificate of Incorporation (COI). There are several important post-incorporation steps every entrepreneur must take to keep the business legally compliant and operationally sound.

Once the company is incorporated, the government automatically begins processing your Permanent Account Number (PAN) and Tax Deduction Account Number (TAN). These are generally received within 7–10 days via post.

To handle business transactions, you need a current account in your company’s name. Documents required include:

This must be filed within 180 days of incorporation for companies with share capital. It confirms that shareholders have paid for their shares.

Penalties: Rs. 50,000 for the company and Rs. 1,000 per day for directors for non-compliance.

GST registration is mandatory if:

Depending on your business activity, you might need:

The first auditor must be appointed within 30 days of incorporation. File Form ADT-1 to notify the Registrar of Companies (ROC).

This meeting must happen within 30 days of incorporation to:

Allot and issue share certificates to shareholders within 60 days of incorporation. Also maintain registers such as:

The company must maintain updated records of meetings, shareholders, and financial accounts. These must be stored at the registered office and be made available upon official request.

While not mandatory, insurance coverage is advisable. Consider:

Annual filings are mandatory and include:

Incorporation is just the beginning. Completing the post-incorporation procedures ensures legal compliance, builds credibility, and avoids future penalties. Partnering with experienced consultants like NeuSource Startup Minds can ease the process, letting you focus on what matters — growing your business.

28 Jul

The internet offers opportunity, but only strategy builds success. Don't just exist online—dominate. Choose Neusource to craft your digital footprint and lead your business to its peak.